45 yield to maturity of zero coupon bond

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Calculating Yield to Maturity on a Zero-coupon Bond YTM = (M/P) 1/n - 1 variable definitions: YTM = yield to maturity, as a decimal (multiply it by 100 to convert it to percent) M = maturity value P = price n = years until maturity Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded semi-annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05/2) 5*2 = $781.20 The price that John will pay for the bond today is $781.20.

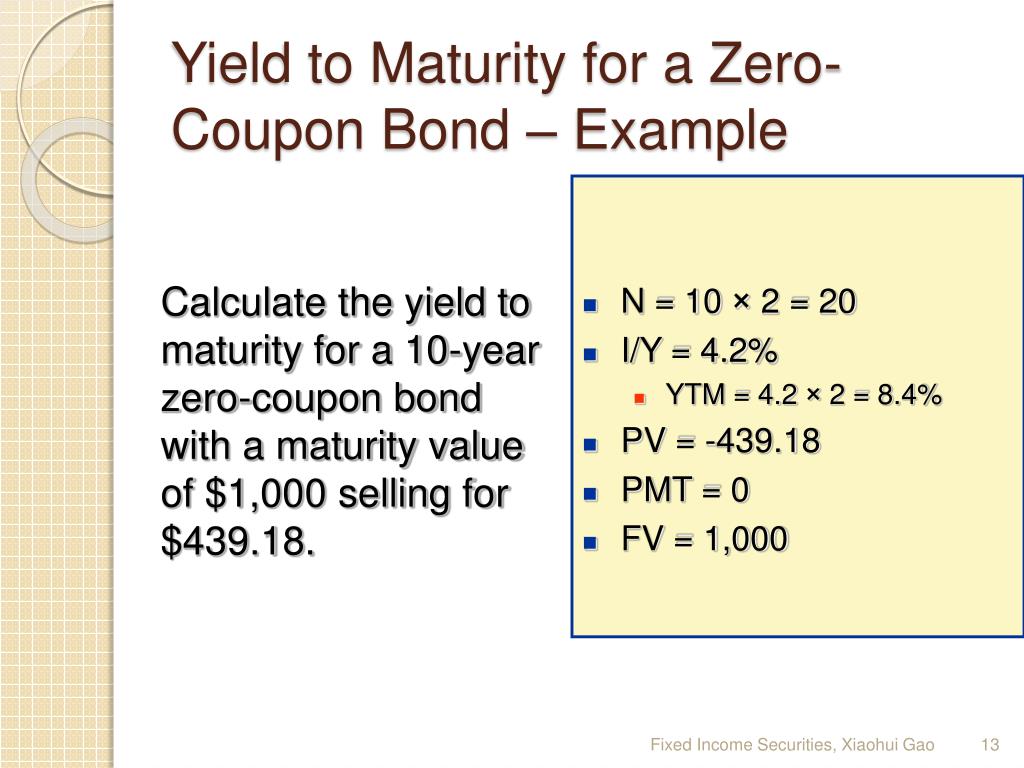

Yield to Maturity (YTM) Definition & Example | InvestingAnswers The estimated YTM for this bond is 13.220%. How Yield to Maturity Is Calculated (for Zero Coupon Bonds) Since zero coupon bonds don't have recurring interest payments, they don't have a coupon rate. The zero coupon bond formula is as follows: Yield to Maturity Calculator

Yield to maturity of zero coupon bond

Bootstrapping | How to Construct a Zero Coupon Yield Curve in ... Zero-Coupon Rate for 2 Years = 4.25%. Hence, the zero-coupon discount rate to be used for the 2-year bond will be 4.25%. Conclusion. The bootstrap examples give an insight into how zero rates are calculated for the pricing of bonds and other financial products. One must correctly look at the market conventions for proper calculation of the zero ... All else constant a bond will sell at when the yield to maturity is the ... 11) All else constant, a coupon bond that is selling at a premium, must have: A) a coupon rate that is equal to the yield to maturity. B) a market price that is less than par value. C) semiannual interest payments. D) a yield to maturity that is less than the coupon rate. E) a coupon rate that is less than the yield to maturity. Yield to Maturity (YTM) Definition - Investopedia Therefore, the current yield of the bond is (5% coupon x $100 par value) / $95.92 market price = 5.21%. To calculate YTM here, the cash flows must be determined first. Every six months...

Yield to maturity of zero coupon bond. Zero Coupon Bond Calculator 【Yield & Formula】 - Nerd Counter The formula is mentioned below: Zero-Coupon Bond Yield = F 1/n. PV - 1. Here; F represents the Face or Par Value. PV represents the Present Value. n represents the number of periods. I feel it necessary to mention an example here that will make it easy to understand how to calculate the yield of a zero-coupon bond. Yield to maturity - Wikipedia Then continuing by trial and error, a bond gain of 5.53 divided by a bond price of 99.47 produces a yield to maturity of 5.56%. Also, the bond gain and the bond price add up to 105. Finally, a one-year zero-coupon bond of $105 and with a yield to maturity of 5.56%, calculates at a price of 105 / 1.0556^1 or 99.47. Coupon-bearing Bonds How to Calculate Yield to Maturity of a Zero-Coupon Bond - Investopedia The formula for calculating the yield to maturity on a zero-coupon bond is: Yield To Maturity= (Face Value/Current Bond Price)^ (1/Years To Maturity)−1 Zero-Coupon Bond YTM Example Consider a... Curve Bond Yield Python - psw.fotovoltaico.catania.it Which is more volatile, a 20-year zero coupon bond or a 20-year 4 -2 I need help with getting lineplot running Bond valuation can be done using an yield to maturity or using a zero yield curve The action in the world's largest bond market also raises the specter of the yield curve eventually inverting, meaning short-term rates would be higher ...

Zero Coupon Bond (Definition, Formula, Examples, Calculations) = $463.19. Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far. Yield to Maturity vs. Coupon Rate: What's the Difference? May 20, 2022 · The yield to maturity (YTM) is the percentage rate of return for a bond assuming that the investor holds the asset until its maturity date. It is the sum of all of its remaining coupon payments. Zero-Coupon Bond - Definition, How It Works, Formula | Wall Street Oasis A 25% return over 5 years is equivalent to 4.56% compounded returns over the five-year holding period of the bond. Calculating the price of zero coupon bond: The yield to maturity formula can be used to calculate the present value of the bond. By rearranging the above formula, the present value of the bond can be calculated as. where, Bond Yield to Maturity Calculator for Comparing Bonds Let's say you buy a 10 year $1000 bond with a 5% coupon. You hold that bond for the next few years collecting your $50 of annual interest. During that time, interest rates fall, and a comparable 10 year $1000 bond now carries a 4% coupon. Your original bond is now a much more valuable commodity, and it can be sold at a premium on the open market.

When maturity of bond decreases duration? The duration of a zero-coupon bond equals time to maturity. Holding maturity constant, ... Duration is inversely related to the bond's yield to maturity (YTM). Duration can increase or decrease given an increase in the time to maturity (but it usually increases). You can look at this relationship in the upcoming interactive 3D app. Yield to Maturity (YTM) - Overview, Formula, and Importance The approximated YTM on the bond is 18.53%. Importance of Yield to Maturity The primary importance of yield to maturity is the fact that it enables investors to draw comparisons between different securities and the returns they can expect from each. It is critical for determining which securities to add to their portfolios. Suppose you purchase a $1000 Face-Value Zero-Coupon | Chegg.com Finance questions and answers. Suppose you purchase a $1000 Face-Value Zero-Coupon Bond with maturity 30 years and yield to maturity 4% quoted with annual compounding. a) Show the bond cash flows on a time line and compute the current price of the bond b) Draw a graph to illustrate how the price of this bond will change as it gets closer to ... Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. That definition assumes a positive time value of money.It does not make periodic interest payments or have so-called coupons, hence the term zero coupon bond.When the bond reaches maturity, its investor receives its par (or face) value.

[Solved] Problem 15-7 The following is a list of prices for zero-coupon ...

How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping As the face value paid at the maturity date remains the same (1,000), the price investors are willing to pay to buy the zero coupon bonds must fall from 816 to 751, in order from the return to increase from 7% to 10%. Bond Price and Term to Maturity The longer the term the zero coupon bond is issued for the lower the bond price will be.

PPT - Chapter 2 Bond Prices and Yields PowerPoint Presentation, free ...

Yield Curves for Zero-Coupon Bonds - Bank of Canada These files contain daily yields curves for zero-coupon bonds, generated using pricing data for Government of Canada bonds and treasury bills. Each row is a single zero-coupon yield curve, with terms to maturity ranging from 0.25 years (column 1) to 30.00 years (column 120). The data are expressed as decimals (e.g. 0.0500 = 5.00% yield). A ...

Zero coupon bond yield to maturity calculator 778066-Coupon bond yield ...

Zero-Coupon Bond Definition - Investopedia Nov 11, 2021 · Zero-Coupon Bond: A zero-coupon bond is a debt security that doesn't pay interest (a coupon) but is traded at a deep discount, rendering profit at maturity when the bond is redeemed for its full ...

How to Calculate YTM and effective annual yield from bond cash flows in ...

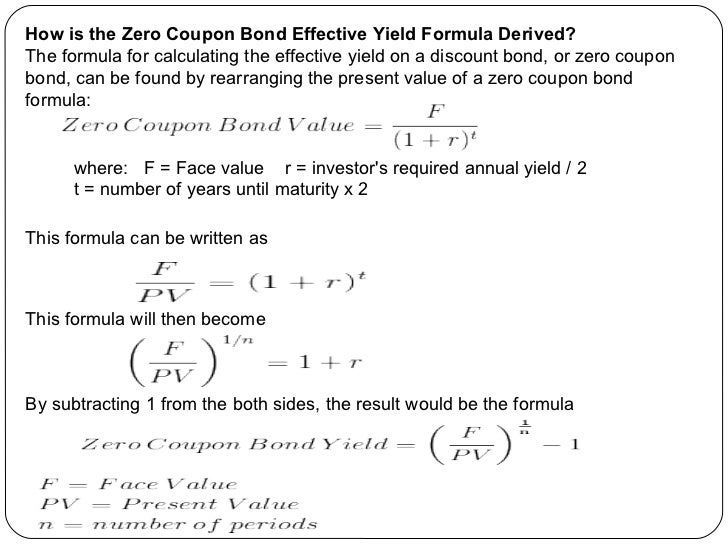

Zero-Coupon Bond: Formula and Excel Calculator - Wall Street Prep To calculate the yield-to-maturity (YTM) on a zero-coupon bond, first divide the face value (FV) of the bond by the present value (PV). The result is then raised to the power of one divided by the number of compounding periods. Zero-Coupon Bond YTM Formula Yield-to-Maturity (YTM) = (FV / PV) ^ (1 / t) - 1 Zero-Coupon Bond Risks

The following is a list of prices for zero-coupon bonds of various ...

Zero Coupon Bond Yield - Formula (with Calculator) - finance formulas The formula for calculating the effective yield on a discount bond, or zero coupon bond, can be found by rearranging the present value of a zero coupon bond formula: This formula can be written as This formula will then become By subtracting 1 from the both sides, the result would be the formula shown at the top of the page. Return to Top

Zero coupon bond yield to maturity calculator 778066-Coupon bond yield ...

YIELDS TO MATURITY ON ZERO-COUPON RONDS - Bond Math - Ebrary However, there is no inherent reason why the annual yield on a zero-coupon bond cannot be calculated for quarterly, monthly, daily, or even hourly compounding. Those yields turn out to be 5.141%, 5.119%, 5.109%, and 5.108% using PER = 4,12, 365, and 365 * 24, respectively. Alternatively, you could convert from any one periodicity to any other ...

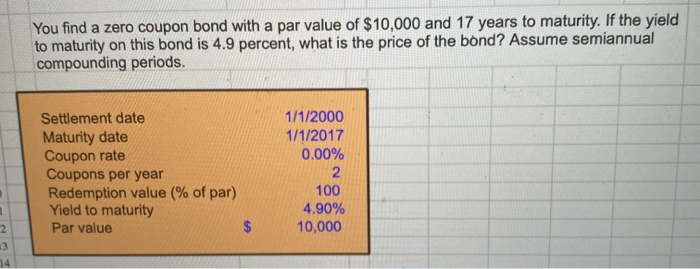

Solved: You Find A Zero Coupon Bond With A Par Value Of $1... | Chegg.com

Bond Yield to Maturity (YTM) Calculator - kili.railpage.com.au This calculator automatically assumes an investor holds to maturity, reinvests coupons, and all payments and coupons will be paid on time. The page also includes the approximate yield to maturity formula, and includes a discussion on how to find - or approach - the exact yield to maturity. Bond Yield to Maturity Calculator

Bonds ppt

Answered: Suppose you purchase a $1000 Face-Value… | bartleby Question. Suppose you purchase a $1000 Face-Value Zero-Coupon Bond with maturity 30 years and yield to maturity 4% quoted with annual compounding. Show the bond cash flows on a time line and compute the current price of the bond Draw a graph to illustrate how the price of this bond will change as it gets closer to maturity - Price (on y axis ...

PPT - Bonds with embedded options PowerPoint Presentation, free ...

Bond Yield to Maturity (YTM) Calculator - DQYDJ Yield to Maturity of Zero Coupon Bonds. A zero coupon bond is a bond which doesn't pay periodic payments, instead having only a face value (value at maturity) and a present value (current value). This makes calculating the yield to maturity of a zero coupon bond straight-forward:

A 12.25-year maturity zero-coupon bond selling at a yield to maturity ...

Yield to Maturity (YTM) Definition - Investopedia Therefore, the current yield of the bond is (5% coupon x $100 par value) / $95.92 market price = 5.21%. To calculate YTM here, the cash flows must be determined first. Every six months...

Bond pricing - Bogleheads

All else constant a bond will sell at when the yield to maturity is the ... 11) All else constant, a coupon bond that is selling at a premium, must have: A) a coupon rate that is equal to the yield to maturity. B) a market price that is less than par value. C) semiannual interest payments. D) a yield to maturity that is less than the coupon rate. E) a coupon rate that is less than the yield to maturity.

Solved: You Find A Zero Coupon Bond With A Par Value Of $1... | Chegg.com

Bootstrapping | How to Construct a Zero Coupon Yield Curve in ... Zero-Coupon Rate for 2 Years = 4.25%. Hence, the zero-coupon discount rate to be used for the 2-year bond will be 4.25%. Conclusion. The bootstrap examples give an insight into how zero rates are calculated for the pricing of bonds and other financial products. One must correctly look at the market conventions for proper calculation of the zero ...

Fixed Income: Spot Rate Calculation – Forward Rate Calculation ...

![[最も人気のある!] yield to maturity formula zero coupon bond 161022-Yield to ...](https://d2vlcm61l7u1fs.cloudfront.net/media/a6d/a6d9a045-4c4d-413c-a5a5-6b37b2d46e5a/phpSMkGD9.png)

[最も人気のある!] yield to maturity formula zero coupon bond 161022-Yield to ...

Bond’s Maturity, Coupon, and Yield Level | CFA Level 1 - AnalystPrep

PPT - Yield Measures PowerPoint Presentation, free download - ID:866185

How did physical bond coupons actually work? - Quora

Post a Comment for "45 yield to maturity of zero coupon bond"